Fixed vs. Variable Mortgage Rates in 2026: Which Is Better?

Mortgage Education | June 10, 2026

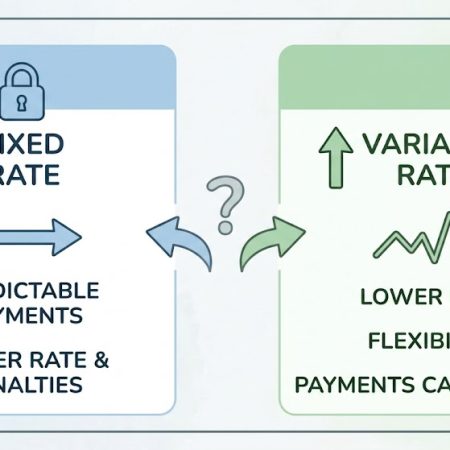

This is one of the most common questions we’re asked right now. The truth is, there isn’t a “right” answer.... View Article

This is one of the most common questions we’re asked right now. The truth is, there isn’t a “right” answer.... View Article

Staying updated on mortgage rates news is absolutely essential for buyers and current homeowners alike. In this update, we analyze... View Article

The 2026 real estate market moves incredibly fast. Therefore, preparing early is your absolute best strategy. Getting a mortgage pre... View Article

The Bank of Canada interest rate has officially held steady at its key policy rate of 2.25%, aligning perfectly with... View Article

Navigating the 2026 Canadian housing market requires a smart strategy. The Bank of Canada is currently holding rates steady. Therefore,... View Article

Navigating the Canadian real estate market requires more than just finding a property you love. To protect your long-term wealth,... View Article