Fixed vs. Variable Mortgage Rates in 2026: Which Is Better?

Mortgage Education | June 10, 2026

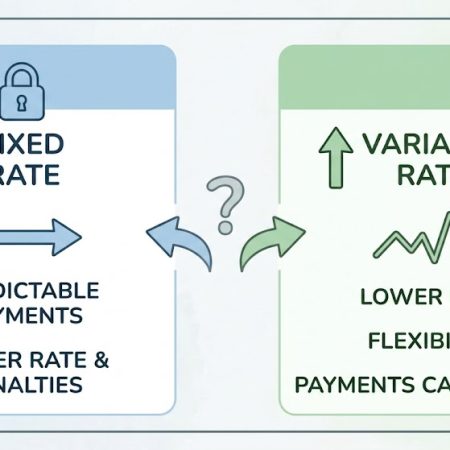

This is one of the most common questions we’re asked right now. The truth is, there isn’t a “right” answer.... View Article

This is one of the most common questions we’re asked right now. The truth is, there isn’t a “right” answer.... View Article

The 2026 real estate market moves incredibly fast. Therefore, preparing early is your absolute best strategy. Getting a mortgage pre... View Article

Navigating the 2026 Canadian housing market requires a smart strategy. The Bank of Canada is currently holding rates steady. Therefore,... View Article

Navigating the Canadian real estate market requires more than just finding a property you love. To protect your long-term wealth,... View Article

Navigating the Canadian real estate market in 2026 requires more than just a down payment; it requires strategic advice. As... View Article

Getting a mortgage isn’t a one-size-fits-all process. With the Bank of Canada holding its overnight policy rate at 2.25%, many... View Article