Bank of Canada Interest Rate News: Spring 2026 Update

The Bank of Canada interest rate has officially held steady at its key policy rate of 2.25%, aligning perfectly with broad market expectations. If you are currently navigating the Canadian housing market, digesting economic news can feel overwhelming. However, keeping a pulse on these updates is crucial for understanding your borrowing costs. Here is a informative breakdown of what is happening in the economy and what it means for your mortgage.

Understanding the Bank of Canada Interest Rate Environment

There is a simple, if somewhat counterintuitive, way to think about today’s economic environment: Bad economic news often equals good news for interest rates. Right now, the Canadian economy is showing classic signs of slowing down. Typically, a weakening economy leads to lower interest rates over time. Here is what is driving that trend:

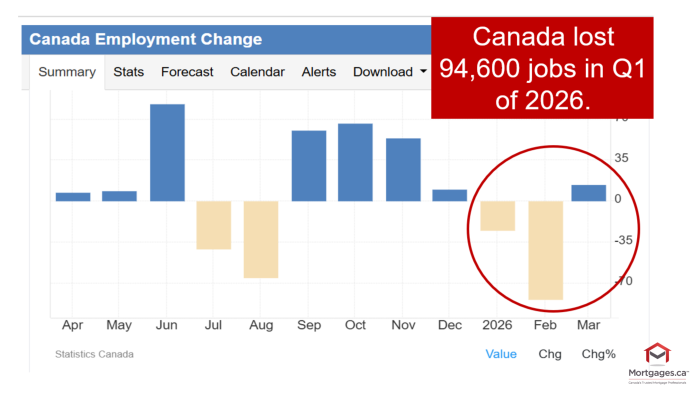

- Rising Unemployment: Unemployment is rising across the country and is likely to increase further.

- Sluggish Growth: Economic growth (GDP) is currently trending negative.

The One Wild Card: Inflation

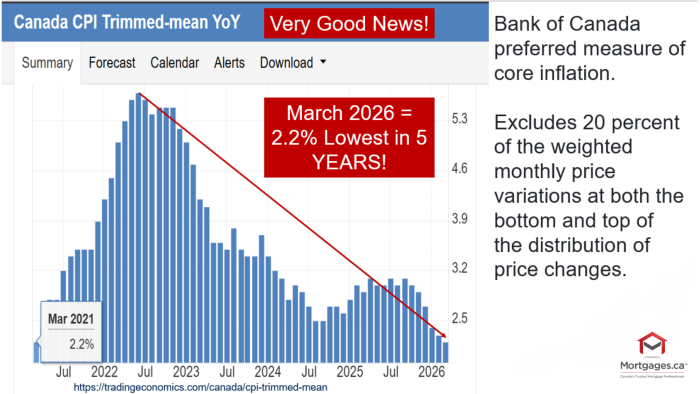

Inflation is the key variable keeping the Bank of Canada interest rate from dropping immediately. High inflation impacts everyone, especially everyday households.

If inflation remains elevated, it can force rates higher. However, the central bank faces a difficult balancing act: it is very difficult to raise rates while the economy is simultaneously slowing down.

The Economic Tug-of-War

To easily visualize the current market dynamics, here is a breakdown of the competing economic forces:

| Factors Signaling Potential Rate Cuts | Factors Signaling Rate Holds or Increases |

| Rising Unemployment: Currently in the 6.5% to 7% range. | Rising Inflation: CPI inflation recently jumped to 2.4%. |

| Slow GDP Growth: Projected at a sluggish 1.2% for 2026. | Global Energy Costs: Oil prices are surging due to conflict in the Middle East. |

| Trade Uncertainty: U.S. tariffs are suppressing business investment. | Sticky Costs: Ongoing housing affordability challenges and elevated food prices. |

Where Are Rates Headed Next?

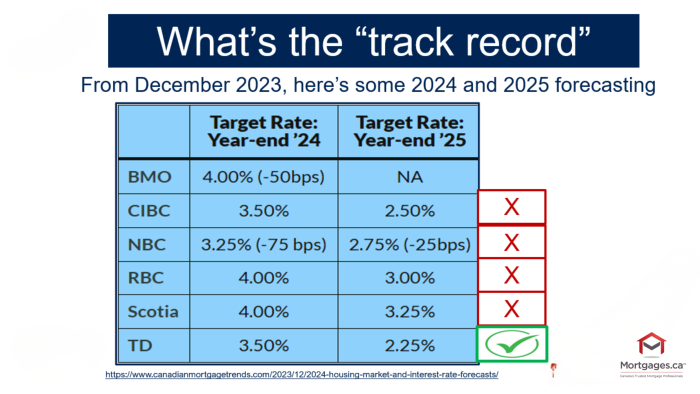

The honest answer? No one knows for certain. Even major financial institutions and banks have been wrong before.

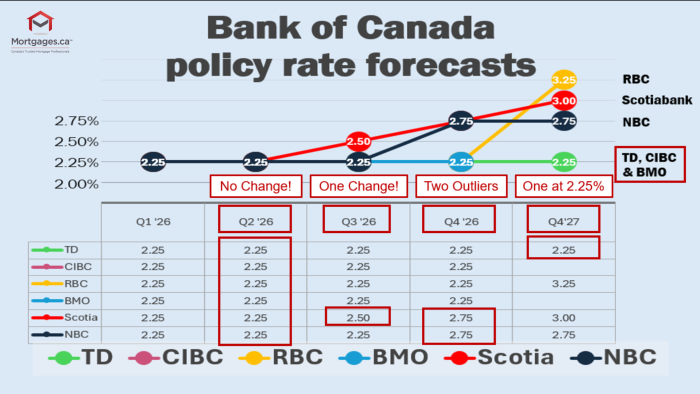

That being said, TD Bank is currently forecasting that the next move is more likely to be a rate cut rather than an increase. The most probable path forward is that rates will remain stable in the near term before gradually shifting lower over time.

Q&A: Your Top Questions Answered

The next scheduled date for the central bank to announce its overnight rate target is June 10, 2026.

It means that strategy matters more than ever. Instead of just chasing the lowest rate, borrowers should weigh the value of flexibility. Because there is currently a premium to lock into fixed rates, you need to decide if that premium is worth paying for peace of mind, or if you prefer a structure that allows you to easily adapt if the market changes.

Final Thoughts

As Yogi Berra famously said: “It’s tough to make predictions, especially about the future.”

In today’s market, the right mortgage structure can save you tens of thousands of dollars over time—not just in interest, but in long-term flexibility and penalty avoidance.

If you would like to review your current mortgage or discuss an informative, personalized strategy, we are always happy to help. Reach out to us at Mortgages.ca. Our goal is simple: to help you make the best decision not just for today, but for the life of your mortgage.